Understanding a HECM Reverse Mortgage Statement

Reverse Mortgage Statements are kind of difficult to understand. They are different from normal mortgage statements and they normally use different terminologies which can confuse most people.

Guide to your HECM Reverse Mortgage Statement:

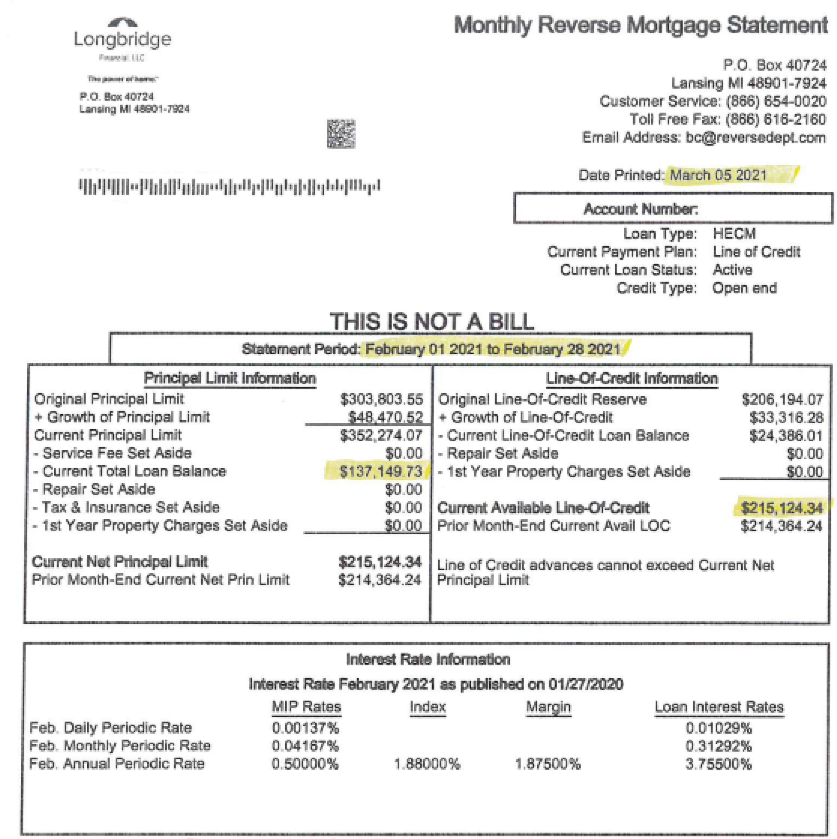

Most of the major banks use the same format for Reverse Mortgage Statements. Below is an example from Longbridge Financial. If your current loan is with AAG, Finance of America Reverse, Celink, Mutual of Omaha, Reverse Mortgage Funding, Liberty, or many other major companies your statement will usually look very much like this one.

I’ve highlighted the elements that are usually most important to you as the homeowner but let’s go through the entire statement to explain what everything means:

Principal Limit Information

Principal Limit: This is essentially your borrowing power or the maximum amount you can borrow with your Reverse Mortgage.

Original Principal Limit: This refers to the Principal limit at the time the loan closed.

Growth of Principal Limit: Because Reverse Mortgages typically grow over time, this growth amount shows how much your borrowing power has increased.

Current Principal Limit: This is the total of the original and growth of the principal limit. Again, showing your current maximum borrowing power/loan amount.

Service Fee Set Aside: Some banks charge a monthly servicing fee but most do not. If your bank does, you may consider calling them to see if you can have it removed.

Current Total Loan Balance: This is the actual balance of your mortgage. This is the amount that must be repaid to the bank if you were to pass away or sell the home.

Repair Set Aside: Although rare, in some cases where a home needs repairs to qualify for a Reverse Mortgage, the lender will allow money to be set aside from the line of credit. This money is used to pay for the repairs so it doesn’t prevent the mortgage from closing.

Tax & Insurance Set Aside: Also known as a LESA (Life Expectancy Set Aside), this is a portion of the Line of Credit that is held in reserve to pay taxes and insurance each year.

Line of Credit Information

Original Line of Credit Reserve: This refers to the total line of credit at the time the loan closed.

Growth of Line of Credit: Any unused portion of the line of credit grows at the same rate as the interest rate and mortgage insurance rates combined. This line is referring to how much the line of credit has grown since the loan was originated.

Current Line of Credit Loan Balance: This line shows how much of the original line of credit has been drawn since the loan closed.

Current Available Line of Credit: This is the amount that could be drawn from the mortgage today.

1st year available Line of Credit: FHA limits the number of available funds the first year. If this line appears on your statement’s just to clarify how much of your Line of Credit is available now and how much will be available after the first year.

Interest Rate Information

Daily Periodic Rate/Monthly Periodic Rate: I don’t know why these figures are included. Most people refer to the annual periodic rate to know how much interest they are charged. But these break it down to a daily and monthly rate.

MIP Rates: This is the Mortgage Insurance Premium Rate that FHA Charges each year.

Index/Margin: These are used to calculate the interest rate when the loan has an adjustable rate. If you have a fixed interest rate you will not have an index or margin.

The Index usually adjusts either once a month or once a year depending on the loan you have. Most lenders today use the Constant Maturity Treasury (CMT) as the index.

The Margin is fixed based on the rate chosen at the time the loan closed.

Loan Interest Rate: This is your real interest rate on the mortgage of what you are charged every year.

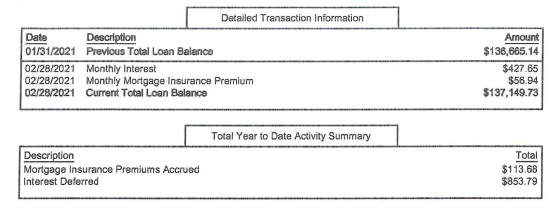

2nd Page

The second page breaks down your actual charges every month for what you were charged for monthly interest and what you were charged for the Monthly Mortgage Insurance Premium.

This is where you’ll look to see how much your loan actually grew from month to month.

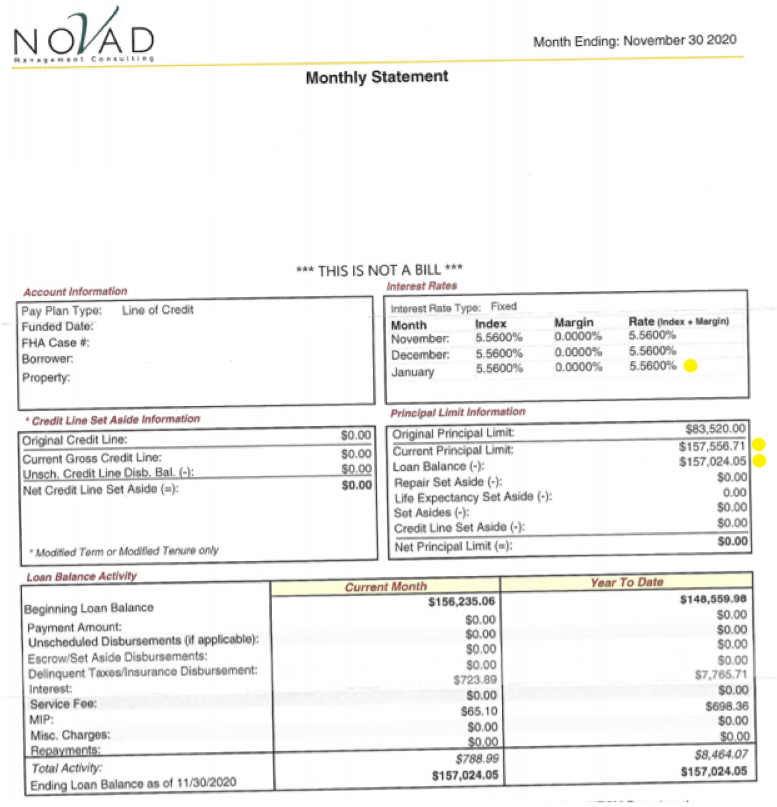

Novad Statements

For those who have had a Reverse Mortgage for around 10 years or more, it is very common to have Novad as your Reverse Mortgage servicer. Wells Fargo at one point was a major producer of Reverse Mortgages but when they decided to leave the industry Novad is the company that stepped in and took over the servicing of most of their portfolio. Below is an example of a Novad Statement and I’ve marked yellow dots next to the key points most people are concerned about:

I hope this breakdown of Reverse Mortgage statements is helpful. If you still have questions or confusion about your HECM Reverse Mortgage Statement please give us a call. We’re happy to answer your questions as best we can, even if we did not originate your mortgage.

Trevor Carlson

President – Reverse Mortgage Specialist

Heritage Reverse Mortgage

435-359-9000

www.heritagereversemortgage.com

Heritage NMLS #1497455 Trevor’s NMLS #: 267962

1060 South Main Street Bldg. A Suite 101B

St George Utah 84770